Long-Term Disability & Social Security

Long-Term Disability / Short-Term Disability And Social Security

This content speaks exclusively to disabled Americans who are presently receiving benefits under a Short-Term or Long-Term Disability plan provided by their employer.

As you read on, there is one overarching theme and take away that we would like you to remember, and it is this:

While the language baked into your Long-Term Disability Plan requires you to make diligent pursuit of Social Security Disability Benefits, the choice of who will represent you, if anyone, is 100% yours and yours alone.

By now, your LTD Insurer (LTD Carrier) may have already been in contact with you about pursuing Social Security. If they haven’t talked about it with you on the phone or addressed it in correspondence, they soon will. We want to make sure that you completely understand that you are legally authorized to initiate and go through the SSDI claim process on your own, or with assistance of your choosing. For many of the reasons we stated in other sections of this website, we absolutely do not recommend that you pursue this process alone.

Your LTD Carrier may have already set you up with a “vendor” who can assist you in this process. Although that choice is yours, we want to let you know that we too are here to assist you in pursuit of a Social Security Disability Claim, and can provide every service or update that your Carrier may need or require. In fact, your chances of winning are better with us than with any vendor you’ll be paired-up with by your insurer. Keep reading!

If they want periodic updates regarding the status of your claim, we have an authorization that you sign allowing us to keep them updated as often as they want. If they want access to your claim profile in Status Star, we can give you a different authorization allowing this as well. This is important because, in 2019 the Department of Labor (DOL) issued new regulations as it relates to the interplay of Social Security and Long-Term Disability. When your LTD claim reaches the Any Occupation phase and we can explain that in detail, your Carrier must account for the SSDI outcome in their analysis. If your Carrier desires, our technology will keep them in compliance with those DOL Regulations. In short, and at each step, we can provide you with competent Attorney Legal representation while keeping you in full compliance with your LTD Plan language.

There will also be no cost to you for our services if we are successful in getting you Social Security disability benefits.

How so? If you are approved for Social Security, and the Agency pays you a lump sum, our fee is credited from the amounts you will owe back to the LTD Carrier under the terms your Plan language. They call this your LTD Plan overpayment. We discuss this in greater detail below.

Although occasionally a Client receiving LTD benefits has told us that LTD staff informed them that they would not cover our fee, this is simply not accurate. In our firm’s 28-years of representing disabled individuals for Social Security Disability benefits, many thousands have been referred to us by insurance carriers. And in all that time, we have never – not even once – had an insurer refuse to pay for our services, and for good reason.

As an American, you have the right to representation of your choosing, and such a statement or any action anyone takes to impede or frustrate that right, would be contrary to insurance regulations in all 50 states. In fact, when LTD Carriers refer clients to us, we ensure that the individual making the referral is made aware that our involvement in the LTD claim is voluntary based on the Client’s decision. If such a restrictive statement has been made to you by any LTD Carrier’s staff, you should call us and let us know.

Here are a few additional things to consider. First, we have been representing disabled Americans who are receiving Long-Term Disability since 1994. Second, we have been in this LTD market for 28 years, and presently work with several LTD Carriers right now. We know each and every ‘advocacy company’ that markets themselves to the LTD Carriers.

Additionally, you want to make sure that you completely understand whether or not the “vendor services” you’re being offered are Attorneys or non-attorney “advocates”. It’s very simple to verify. They have or should be sending you a form called an SSA-1696 (Appointment of Representative). This signed document is required by Social Security Regulations before you can actually have someone assist you in your Social Security claim.

In August of 2020, the Agency updated the SSA-1696. We will show you the old version and the current version of the form. If you can, stop here to take a moment to look for the SSA-1696.

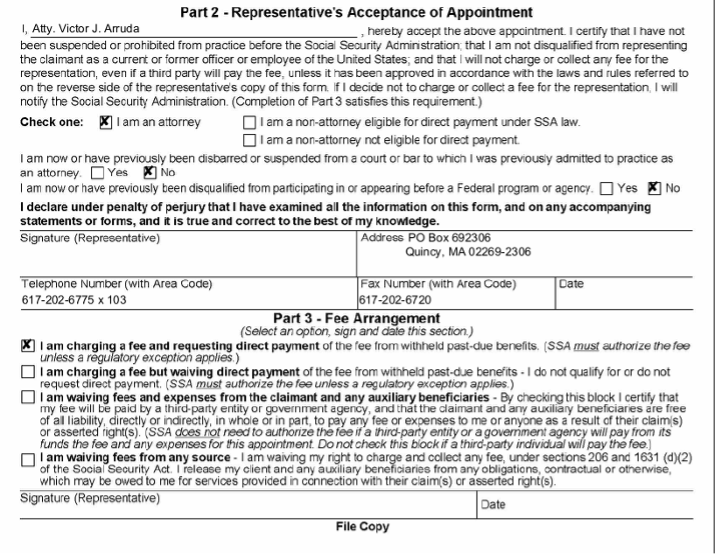

In the old version of the form which may still be in circulation (below), that question is answered in Part 2 of the 1696. As you can see, the Social Security Law Group is a Law Firm comprised of Attorneys who provide Legal Services. If the “vendor” that your LTD Carrier is recommending has sent you a 1696, check Part 2. If the Attorney box is not checked, then by definition, they are non-attorney “advocates”. It would be a violation of SSA Regulations and state Bar rules to check the Attorney box if one is not a Licensed Attorney. We didn’t pay thousands of dollars and endure 3+ years of hard work to have it diluted by checking a box.

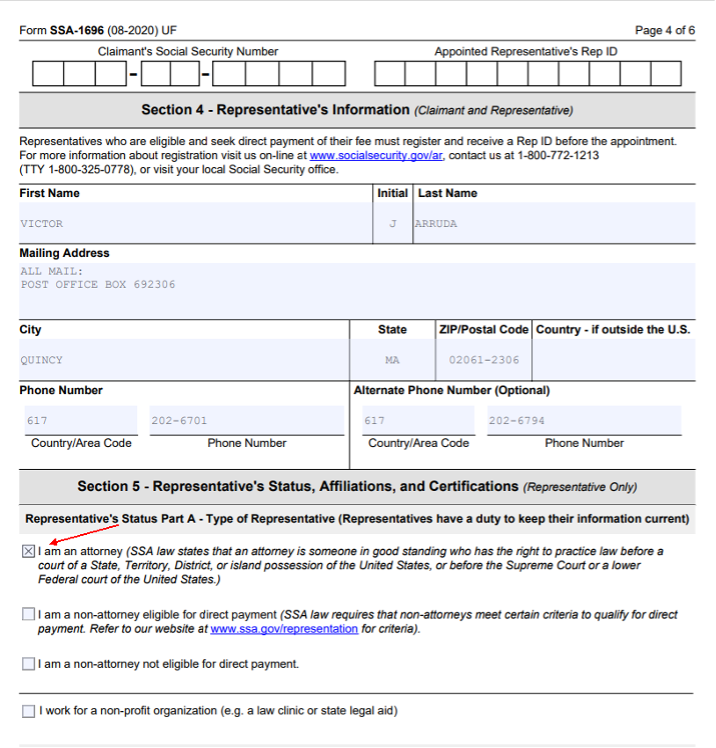

In the new 2020 version of the form, you’ll find the answer to that same question in Section 5:

What’s the difference you might ask? The difference is gargantuan! While the SSA regulations allow non-attorneys to represent clients before Social Security and collect a fee from your Past Due benefits, our skill, preparation, knowledge, and respect from the ALJ’s cannot be matched, plain and simple. The Social Security Law Group has one of the best reputations throughout the SSA, DDS’s and OHOs. The companies in this space know it, and we do too. In addition, as Attorneys, you are granted additional rights and protections by your state’s laws as they relate to the Attorney-Client relationship. Those same laws do not apply to non-attorney “advocates”.

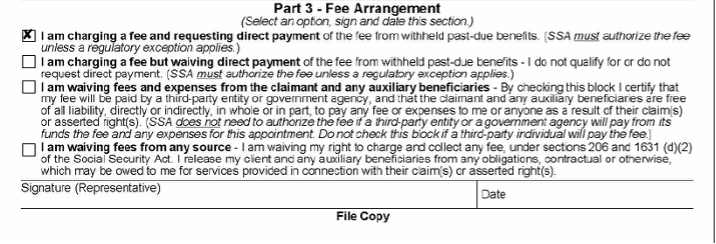

Let’s take the fee arrangement as a prime example, you’ll also find the fee arrangement in that same 1696 Form. In the previous version, it is contained in Part 3.

As you can see above, our fee is paid by the Social Security Administration. It must be first approved by the Agency and then it’s sent to us. You then receive the remainder of your Past Due Benefits. When your LTD Carrier sends you an invoice for your overpayment, they will deduct the amount that we’ve been paid from what you owe them. (See illustration 4)

In many cases, the “vendor” that your Carrier is recommending will be checking the third box down (3). This means that the Agency will release all the Past Due Benefits to you, and then you will owe the money back to the Carrier. The vendor will either send the Carrier an invoice for their services, or they will offer to recover your overpayment and remove the agreed-upon fee prior to sending the remainder of the funds back to your LTD carrier.

As attorneys, if we were to make such an arrangement with your LTD Carrier, we are required by regulation to explicitly and clearly disclose these details to you, our Client. The regulations requiring this disclosure is for your benefit. Non-attorney “advocates” have no such requirement. In addition, if we assist you with any repayment efforts back to your Carrier, other States’ Bar Regulations require us to do this through our Client Trust Fund Account (IOLTA). These accounts are certified by the state and heavily regulated by the state Bar Associations in all 50 states. These regulations are also for your protection. Once again, non-attorney “advocates” have no such requirement.

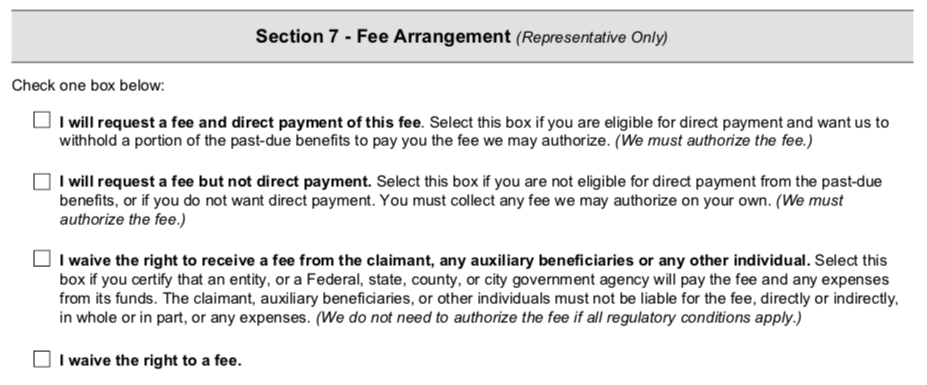

In the August 2020 version of the Form-1696, you’ll find that arrangement in Section 7.

Call us today at 800-909-SSLG

While these details may seem minor or trivial, we believe they are important protections that are afforded to you in the Attorney-Client relationship. Unfortunately, we haven’t even addressed the starkest difference between the Social Security Law Group and the “vendor services” that are being recommended to you. That distinction plays itself out on one of the most critical days of your life. Your SSA Hearing before an Administrative Law Judge.

While the Social Security Law Group will assign your case to a Client Services Representative who serves as your day-to-day contact, on demand, you can speak to one of our staff Attorneys at any time. In addition, we give you exclusive access to a host of multimedia preparation modules in which our Attorneys explain the SSDI process, SSA forms, the nuances of your Long-Term Disability Plan in excruciating detail. We will cover issues with you like the Work History Report, Function Report, definitions of Disability under your Group LTD plan language, the requirement to repay your Carrier monies advanced etc.

But when your case reaches a hearing, this is where the rubber truly meets the road. All of these non-attorney “advocates” will “farm out” your ALJ hearing to an attorney in their ‘network’. Some Attorney “vendors” may also do it. Buyer Beware! A farm-out to a Per-Diem lawyer is not the same as having a staff Attorney from the Social Security Law Group prepare you and represent you in front of the Judge.

Since lawyers cannot accept a payment arrangement in which they are paid based on the outcome of the case, the appropriate way for them to be compensated without running afoul of their state’s regulations is something called an Appearance Fee. An Appearance Fee is what happens when these non-attorney “advocates” farm out your case to one of the Attorneys in their ‘network’. The Appearance Fee is a fixed sum paid to the attorney win or lose, and not based on the outcome of the hearing.

We know for a fact, that this fee ranges between $500 and $750 per case. This fee does not include any of the Attorney’s travel expenses. Those are to be absorbed by the Attorney accepting the case. One of our staff Attorneys confirmed it as low as $350.00. How do we know? Our attorneys have been pitched in the past to accept this arrangement and join the ‘network’. We know at one time, there was an auction for the hearing, with the lowest bidder getting the case.

Let’s get back to the disclosure we’ve been talking about. We suspect that in the packet of forms you’ve been asked to sign, there isn’t one that is explaining to you in any intelligent way the details of how this arrangement will work if your case goes to a ALJ Hearing. As Attorneys, we can’t side-step this step. All our Clients sign a document that we call the Attorney-Client Memorandum of Understanding. This document will clearly explain how we will process your case, and remind you of your obligation to repay any resulting LTD plan overpayment to the Carrier in the event your case is approved by SSA.

Some of our attorneys have been doing this work for over 20 years. We cannot imagine adequately preparing and giving the time, attention, and detailed analysis that each and every case deserves at a $700 appearance fee. And remember, that’s on the high side of the scale!

So if you are receiving Long-Term Disability and you have not yet applied for Social Security, give us a call. We will give you a free assessment of your case, and whether or not we believe an SSDI claim has merit. If you have a case pending and you’re simply not happy with the services or the attention you’re getting, give us a call. We will gladly give you a free consultation. Once again, you are always free to get the representative of your choosing at any time during the claims process.

Here are several examples of how our fee works, and how there is no cost to you. In each example, your SSA Past Due Benefits are $10,000.00. While any Cost of Living Adjustments (COLAs) paid by SSA are yours to keep, to make it easy to understand how our fee works, we’ve set your Overpayment at $10,000.00 as well. The Net O/P in the examples below is the amount you would owe back to your Carrier under your Plan Language.

1-In this example, here’s how it works if you won the case without any assistance from anyone:

| SSA PAST DUE $$ | SSLG’s FEE | Amt SSA pays you | Carrier Gross O/P | Atty Fee Credit | Net O/P |

|---|---|---|---|---|---|

| $10,000 | — | $10,000 | $10,000 | — | $10,000 |

As you can see, there is no incentive for you to navigate this SSA Claims process on your own. You gain no financial advantage. Those SSA funds are owed back to your Carrier under the Plan Language anyway, so why risk it and jeopardize your case? We see it happen all the time. Don’t let it happen to you.

2-In this example, here’s how it works if SSLG assists you:

| SSA PAST DUE $$ | SSLG’s FEE | Amt SSA pays you | Carrier Gross O/P | Atty Fee Credit | Net O/P |

|---|---|---|---|---|---|

| $10,000 | $2,500 | $7,500 | $10,000 | $2,500 | $7,500 |

As you can see from the example above, any funds SSA pays us are deducted from your Overpayment. The net amount you owe has been adjusted to take into account what SSA paid us. When your Carrier sends you a letter concerning the Overpayment, they will have deducted and credited our fee. This is what we mean by no cost to you.

3-In this example, here’s how it works if the Carrier’s recommended “vendor” assists you:

| SSA PAST DUE $$ | Vendor’s FEE | Amt SSA pays you | Gross Overpayment | Vendor Fee Credit | Net O/P |

|---|---|---|---|---|---|

| $10,000 | $2,500 | $7,500 | $10,000 | $2,500 | $7,500 |

Just like in the SSLG example above, any funds SSA pays the “vendor” are deducted from your Overpayment. The net amount you owe has been adjusted to take into account what SSA paid the vendor. This is what they mean by no cost to you.

4-In this final example, here’s how it works if the Carrier is going to pay the “vendor” fee directly either at the conclusion of the process, or after “sweeping” your account:

| SSA PAST DUE $$ | Vendor’s FEE | Amt SSA pays you | Gross Overpayment | Vendor Fee Credit | Net O/P |

|---|---|---|---|---|---|

| $10,000 | — | $10,000 | $10,000 | — | $10,000 |

In this example above, the vendor either sent the entire $10,000 to your Carrier after sweeping your account, or removed their agreed upon fee and sent the balance to your Carrier. As you can see, no matter what the arrangement, SSLG’s Legal Services have no effect on the amount you’ll owe back to your Carrier under the terms of your Plan Language.

I am still working, but not doing so well what are my options?

If this is your situation, we are happy that you are reading this content now, rather than when it’s too late. If you’re still working but are struggling, missing time, leaving early, reassigned etc., you may not be long for your job, or at least Full-Time.

Our recommendation is that you contact your Human Resources department, and ask if your Company has Short or Long-Term Disability as part of the benefit package. The fastest way is to review your last paystub, you should see a deduction for Long-Term Disability or Short-Term Disability. It might also be listed under company benefits.

Either way, it’s worth a quick call to the HR department to determine if you have Short-Term disability. Some companies offer Short-Term, but not Long-Term. Our recommendation is that if you are going to stop working because of a medical condition, you should coordinate that through your HR department so that if you do have this coverage as part of your benefit plan, you can apply for Short-Term disability as you take the time off to convalesce.

We have plenty of clients who didn’t realize they had this benefit, quit because of a medical condition, and are no longer able to file a Short-Term or Long-Term Disability claim. Don’t let that happen to you. If you’re not sure, call your HR department and ask.

Another Representation Vendor is assisting me. My SSDI case is pending, but I am just not satisfied with the service I’m getting.

Under SSA regulations, you are free to select a different representative if you believe the one you currently have is not meeting your expectations. We are certainly here to lend an ear, and will gladly assess your case and whether or not you should continue or make a change.

If your case is pending a hearing, we will definitely recommend pulling that trigger prior to the hearing. If it’s at one of the earlier levels of the SSDI claim process, we may advise you to wait until that part of the claims process has concluded. Either way, we are more than happy to assess your case and discuss your options. The choice is always yours, and our consultation is free.

Now you may be asking yourself…

I paid these premiums every week! What gives?

What’s in it for me?

Why am I doing this?

There appears to be nothing in it for me.

That’s not 100% true. While the LTD Plan language requires you to file a claim, and repay that money if you’re approved, that particular repayment Clause is reflected in the weekly premiums you paid as an employee. In most cases, your employer matched your weekly contributions and that kept premiums down to an affordable level.

Believe us, we have had hundreds of Clients who aren’t lucky enough to have Long-Term Disability benefits and have to navigate this process with no income at all. Other Clients opted out of Long-Term Disability and now regret it. For those SSLG Clients, having zero income while their cases languish at DDS or the SSA Hearing Office is especially difficult on them.

Many of our Clients who have qualified for Food Stamps or other government benefits are required by State regulation to repay those benefits out of their Social Security awards as well. In fact, the Agency will suck those funds right out of their Past Due Benefits and send the Client the balance. While we understand the frustration, you have to realize that those premiums were affordable precisely because your LTD benefits coordinated with these other benefits, including Social Security Disability.

In addition, if you’re approved for Social Security, the government will give you a Cost-of-Living Adjustment every January. Group LTD Plans do not reduce (or “offset”) for COLA increases. In other words, those annual COLA’s are yours to keep. Over the past 25-years, Social Security Disability COLAs have averaged 2.8% annually. So over time, these increases add-up!

Many of our Long-Term Disability Clients are no longer covered by their Employer’s health plan. They either have coverage through their spouse, or are paying an exorbitant amount per month in COBRA premiums. If you are approved for Social Security, you will be eligible for Medicare two years from the date of your first monthly benefit. This is especially important for our clients and their health coverage.

We bet you didn’t realize that your Social Security Retirement benefit is based on your annual FICA contributions during your working years. Once you qualify for Social Security Disability, your earnings record is “frozen” and any of those quarters in which you were considered disabled by SSA are not adversely diluting your FICA bank. By qualifying for Social Security Disability, you’re not penalized for no longer contributing to FICA, so your Social Security Retirement benefit will be higher than it would be if you stayed on LTD and didn’t contribute anymore. Since the Government has increased the Retirement age, this is especially important for our clients between the ages of 45 and 65.

Finally, once you’re approved for SSDI, you’re no longer considered a Social Security Claimant, but a Social Security Beneficiary. As a Social Security Beneficiary, there are tremendous incentives in returning to work like the Nine-Month Trial Work Period, Expedited Reinstatement etc. We explain all these in our Post-Award information modules that you can stream on your phone or tablet long into the future.

So while you may not like the language under your plan which requires you to apply and return those advanced monies, these are legal and enforceable provisions that were instituted to keep premiums down. We cannot control those.

Before you go, we’d like to leave you with one final thought that we hope you’ll remember. Your Long-Term Disability plan has two phases. You’re in the midst of phase one which is commonly referred to as the own occupation phase. This means that as long as you cannot perform each and every element of your job as it existed at your company under the job description provided by your HR department, you remain disabled under the Long-Term Disability Plan.

After two years, phase two begins. Beginning in month 25, you have the burden of proving that you are disabled from any occupation as it’s commonly known under the LTD Plan language. Some Carriers call it the any occ phase. Other Carriers call it “test change”. Labels and terminology aside, in short order, these decisions become a very critical part of your life and your future.

If the ALJ denies your claim, we believe it will be much more difficult for you to prove that you are disabled from any occupation, given that the Agency just made an official finding to the contrary. Don’t let someone farm-out your future.

And while we cannot control how the Long-Term Disability Carrier will evaluate and make that determination at phase 2, this is where we say over and over…. don’t chance it. Get the professionals who know the landscape as good or better than anyone involved in your SSDI Claim now.

What we can control is exceptional customer service and competent Legal Representation. Our goal, of course, is to have you HIRE US to help you qualify for Social Security Disability. We promise you it will be the best decision you’ve ever made.